This section encompasses a wide range of GVC related information:

- "Interview" covers both face-to-face interviews and quotations in third party articles.

- "Publications" includes articles, papers and studies.

Friedrichskoog, October 2025

Wolfgang published an article titled “Keine Zeitenwende bei der Energiewende” (No turning point for the Energiewende), subtitled “Nicht Systemkostenoptimierung, sondern nur die Änderung des unbezahlbaren Systems führt aus der Sackgasse“ (Not optimization of system costs, but only a change of the unaffordable system as such will lead out of the dead end).

The article picks up on a study supposed to assess the status of the German “Energiewende” requested by the German Ministry of Economics and Energy and the Ministry’s conclusions thereof in a paper named “Schlüsselmaßnahmen” (key action points).

Wolfgang expresses strong disappointment in various respects:

- Already the instructions for the study fell short of an affordability assessment, condemning the authors to restrict themselves to system cost optimization.

- The Ministry did not have the courage to trash the German ambition to be climate neutral 5 years earlier than the European Union, costing triple billions with no climate effect at all.

- The Ministry, with only minor adjustments, confirms the targets for renewables prescribed by law in centrally planned economy fashion, although wind and solar are the root cause for the excessive system costs.

Thereby, the Ministry loses sight not only of affordability and security of supply, but also the state budget limitations. Hence, no “Zeitenwende”, but rather a “Weiter So” (business as usual continued) with only a few tugs here and there as to system costs.

This indicates that Germany would continue its “ghost ride” (Prof. Hans-Werner Sinn), namely shutting down all dispatchable generation sources and relying almost entirely on the weather (wind and solar).

Wolfgang recalled that solar featured a secure load of zero % and wind 1% (onshore) resp. 2% (offshore). Production is oscillating and does hence not contribute to retain grid stability at 50 Herz (<47.5 or > 51.5 Herz means black-out). Moreover, the output relative to the installed capacity is 10% for solar and 20 % for wind. Conversely, a power grid would be underutilized by 90% (solar) and 80% (wind) and consequently uneconomic.

Due to the oscillation within day and also zero production e.g. at the so-called “Dunkelflaute” (no wind, no sun) Germany is affording itself two systems for one supply purpose. The mostly fixed remuneration for wind and solar operators (causing losses for the grid operators if market prices are below such) amounted to 18.5 billion € in 2024. Moreover, at times of Dunkelflaute the so-called “re-dispatch” takes place: Supposedly retired coal-fired power plants, declared system relevant by the regulator (also these costs feeding into the grid costs), are then activated. If that does not suffice, the G-7 industrial state Germany is importing power from the neighbors.

It is a fallacy to believe that the “continued further expansion” of renewables would solve these problems. While the complete German load requirement amounts to ~80 GW, Germany avails meanwhile of ~260 GW of generation capacity, thereof 70 GW wind and 100 GW solar. Expanding these capacities further (the German Renewable Energy Act prescribes – in centrally planned economy fashion – a target of 300 GW solar) will do nothing to overcome their poor output relative to capacity.

The Ministry remains silent on the black-out risk by means of “Hellbrise” (both strong wind and sun): While wind turbines can be curtailed, 100 GW of solar hitting the grid could create an overload of the system and hence a black-out. While Germany sits in the middle of Europe and can thus export surplus into various neighboring states (at negative prices), it is overlooked that all neighbors have installed shutters at the interconnectors which will be activated when the grid stability of any such neighbor is affected.

While there was an inflation of further studies around the assessment report, only one study had the courage to name the full cost of the German Energiewende if continued as is (4 to 5 trillion €) and also that the current system would lead into an economic dead end (“volkswirtschaftliche Sackgasse”).

Attempts to overcome the shortcomings of the current system are mostly unfit to do so and/or very expensive. Wolfgang mentions the much discussed “large” batteries as an example: they avail at best of a storage capacity for two hours and would increase the grid costs substantially while having minimal effect. He also points out that the grid operators are confronted with more that 130 grid connection applications totalling a capacity of ~500 GW (!). Wolfgang calls them “war profiteers”: The traded power market features unseen volatility ranging from negative prices greater than minus 100 €/MWh (at which Germany exports) and scarcity prices up to 1,000 €/MWh and more (at which Germany imports). If I can buy and store at minus 100 €/MWh and withdraw and sell at up to 1,000 €/MWh, profit is guaranteed even at a few 100 hours in the year.

Wolfgang also criticizes the Ministry for adjusting future power demand (which, so the Ministry, reduces the need for grid expansion). It is already scandalous that demand decline due to de-industrialization is factored in. The major flaw however is that the Ministry looks at annual volume (in TWh) instead at the peak load requirements. E.g. 1,000,000 loading stations at 22 kW would increase Germany’s load requirement from 80 to 102 GW (!), not to mention heat pumps.

In this context, Wolfgang also criticizes the various studies (but also the regulator in its recent security of power supply report) that the load from “future additional power users” is treated mostly as “flexible load”, i.e. only used in case of attractive price signals. Moreover, especially the regulator seems to take it for granted that the industrial “load shedding” will continue. Load shedding means that e.g. an aluminum producer stops producing and resells its previously purchased power (at attractive prices) into the market. It appears more than doubtful whether the affected industry will tolerate such practice forever or rather consider to leave Germany and produce elsewhere.

Wolfgang indicates examples of measures, which would drastically change the system and make it affordable, without giving up the climate goals. I.a.:

- Shifting the “coal-exit” by 15 years and continue coal-fired power generation with the use of CCS. This would reduce the costs of CCS by the scale effect, while further savings can be achieved by using on-shore exploited reservoirs rather than off-shore reservoirs or even exports at much higher costs.

- Build additional gas-fired power plants and introduce a capacity market to attract investment. The extension of the coal exit will alleviate the ambitious timing on additional gas-fired power plants.

- Squash any remuneration for new wind turbines as well as the “must-run” privilege: 25 years after market entry, further subsidies cannot be justified any more.

- Obligate operators of existing solar installations to take their facility off the grid if ordered by the grid operator in case of “Hellbrise” without compensation.

- Support research and development in means of climate friendly energy generation which would not need extended subsidies.

It is clear that these and other measures would create massive protest from the green corner and the renewables lobby organizations. On the other hand, Germany would end its “gost ride” and surely earn international respect for now aiming to achieve European climate goals in pragmatic fashion free from ideology, which would also help to turn the German economy around again.

The Ministry remains entirely silent on the affordability and security of supply of natural gas, although its intention is to have up to 20 GW of new gas-fired power generation facilities built and also industry and households will be needing gas for quite a while.

Wolfgang proposes i.a. the accelerated exploitation of German indigenous reserves and resources by use of environmentally friendly fracking:

- The previous environmental concerns were ruled out by the so-called “Fracking Commission” already in 2022, with no action taken by the previous green minister.

- The reserves and resources could cover Germany’s entire demand for many years, perhaps decades.

- Since the Russian gas supply volumes fell away, Europe is competing with e.g. Asia and Latin America for LNG in the global gas market at elevated prices. Accordingly, the price setting European TTF trades at >30 €/MWh even at the current times of modest global demand.

- Significant indigenous production would very likely bring the TTF down again near pre-crisis levels of <20 €/MWh.

- While Norway is undoubtedly a reliable partner, there is a concentration risk as to its infrastructure (e.g. by pipeline sabotage).

- The supply of American LNG has significantly increased, but bears the risk of erratic measures or even blackmail by the unpredictable American President.

- Moreover, the replacement of U.S. LNG by indigenous production would significantly reduce the carbon footprint: Much of the U.S. gas is exploited by open-cast mining with substantial methane emissions.

Heide/Friedrichskoog, June 2025

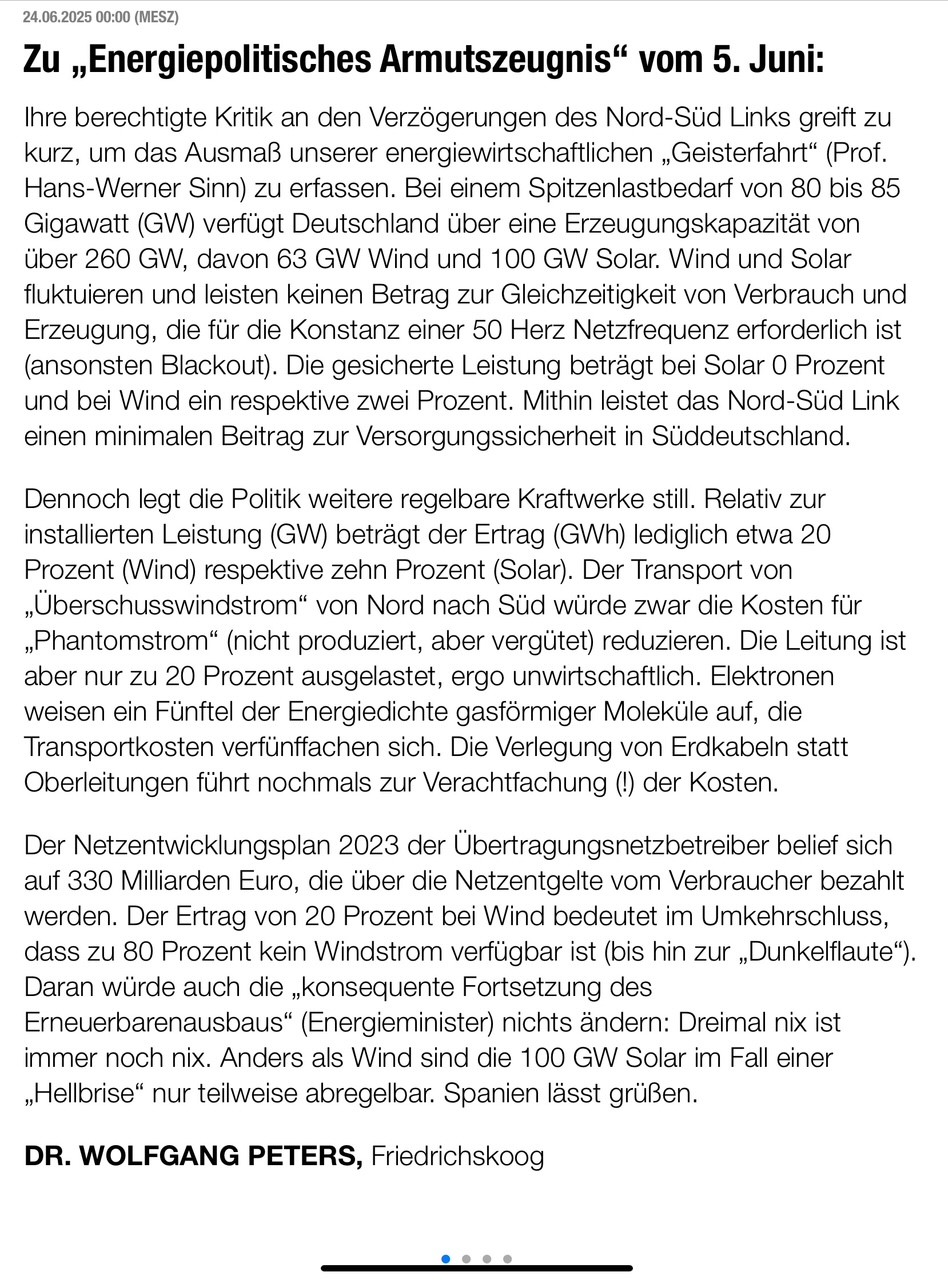

Wolfgang delivered a “Leserbrief“ (reader’s commentary) in the ‘Dithmarscher Landeszeitung’, the leading North-German Newspaper residing in Heide, in response to an article titled ”Energiepolitisches Armutszeugnis” (pathetic display of incapacity in the energy policy space). The journalist criticized the delay of the North-South power link supposed to bring renewable electricity from North to South, which is the cause for wind turbine curtailments for which compensation is eventually payable by the end users.

Wolfgang agreed with the sloppy project management, but pointed out that the extraordinary expensive power link (increasing once more the grid costs payable by the consumers) will contribute minimal additional security of supply (1 to 2%) for the South. Moreover, it is, with an underutilization of 80%, uneconomical, due to the output of wind turbines relative to the capacity installed being only 20%.

{kind=link}

Leipzig/Friedrichskoog, 02 December 2022

Wolfgang was interviewed by the Themen!magazin, a reputed German magazine on energy and energy policies. The interview is titled “Entlastungspakete mildern Symptome, kurieren aber keine Ursachen“. In essence, the interview is an ‚in a nutshell’ version of the ‘Gastkommentar’ in the Handelsblatt newspaper.

Berlin/Friedrichskoog, 19 October 2022

Wolfgang delivered a ‚Gastkommentar‘ (guest commentary) in the Handelsblatt, the leading German business newspaper, titled “Auf heimische Ressourcen setzen” and subtitled “Entlastungspakete mildern nur die Symptome. Deutschland sollte die eigenen Energien nutzen: Strom aus Atom- und Braunkohlekraftwerken sowie Gas durch Fracking.“

For perspective, Wolfgang illustrates that, at traded prices in October 2022, the entire German gas demand 2023 would have cost € 209 billion. Hence, the debt financed € 200 billion subsidy would melt like snow in the sun in a very short time while the elevated prices would persist. Read moreThe root cause for the elevated prices for both gas and electricity is a supply shortfall. This would neither be alleviated by the construction of LNG terminals nor by the accelerated expansion of renewables. Rather, the mobilization of indigenous resources in ‘Kriegsmangelwirtschaft’ fashion would calm the traded markets. This should include the extraction of the huge indigenous German gas resources by environmentally friendly fracking, the continuation of nuclear power generation and CO2 neutral power generation with cheap indigenous lignite by applying the so-called CCS (carbon-capture-storage) technology, the latter strongly recommended by the World Climate Council (‘IPCC’).

Heide/Friedrichskoog, in March 2022

Wolfgang’s resignation from the supervisory board of Gas4Europe was reported in the ‘Dithmarscher Landeszeitung’, a North-German Newspaper residing in Heide, in an article titled “Dithmarscher steigt bei Nord Stream 2 aus”. Wolfgang was quoted as taking this step entirely for moral reasons. For further details please refer to News & Events.

London/Friedrichskoog, 31.01.2022

Wolfgang was interviewed for and quoted in an article titled ‘Europe’s policies aimed at phasing out long-term supply contracts expose midstream suppliers to global price volatility’ by Katya Zapletnyuk, editor in chief of and energy expert at ICIS Heren, published in ICIS Gas In Focus (GIF 29.02 of 31 January 2022), the leading gas industry report with an established audience of executives, analysts and traders since 1994.

The article has been shared by Katya and can also be accessed at https://www.linkedin.com/posts/katya-zapletnyuk-b15645_icis-gasmarket-gassupply-activity-6894302411536547840-S2zY.

Wolfgang pointed out that, while producers were of course entirely capable to offload their entire production into the liquid traded markets by themselves, it created a significant financial burden to come up with the trade margin collateral and also to bear the entire counterparty default credit risk. In the past, after price revisions had established hub-indexation in long-term contracts, various producers had indeed taken some volumes out of the long-term contracts in order to market them by themselves. However, the bulk was left in the long-term contracts with the midstreamers, for the above reasons, the latter now essentially acting as service providers. It was entirely possible that producers might take an initiative later with a view to retain, albeit hub-indexed, long-term contracts.

Brussels/Friedrichskoog, 26.01.2022

Wolfgang was interviewed by the Brussels based ARD journalist Michael Grytz for a news report ‘Wie sicher ist die Gasversorgung ohne russisches Gas’. The report was broadcasted by the ARD, one of the major German news channels in ‘Tagesthemen’ on 26 January 2022 at 22:15 hrs.

I.a., Mr. Grytz pointed out that a serious European pipeline gas supply shortfall was stemming from the decision of the Dutch government to reduce – and eventually finish, as soon as 2022 – the once significant supplies from the giant Groningen field. Indeed, the new German Minister of the Economy, Mr. Harbeck from the Green Party, had visited his Dutch colleague asking to keep the tabs open. Wolfgang pointed out that, while the Media were focusing on Russia shutting down supplies, it appeared, in the face of grim statements of European and American politicians, equally possible that Europe might put an embargo on the import of Russian gas. In both cases, the question was the same, namely whether Europe’s security of gas supply could nonetheless be maintained. Wolfgang pointed to multiple earlier publications and statements that there was meanwhile enough destination-flexible LNG in the global gas market to satisfy European demand. Moreover, there was ample European LNG-regasification capacity to absorb such. However, absent significant pipeline supplies, Europe would directly be competing with Asia for LNG, which could easily drive prices even higher than they already were.